Generative AI will likely transform the global economy, but we will have to be patient

Generative AI has the characteristics of a General Purpose Technology, a rare technology with the power to transform household and business life, bringing significant economic benefits. We should be excited about its potential to drive productivity growth, but at the same time recognise that it will not mean a quick reversal of the current low trend productivity growth . The experience of previous General Purpose Technologies suggests that benefits at an aggregate level could take decades to materialise.

The promise of Generative AI as a General Purpose Technology

Generative AI burst into public consciousness in November 2022 with the public launch Chat-GPT; an AI based tool able to have human-like conversations, answer questions, suggest holiday plans, write essays, code, poems or emails based on natural language prompts. Other organisations developing similar models (Google, Meta, Anthropic, Hugging Face) quickly followed suit by making their similar tools available for public use, including models which can generate images videos and music along with computer code from natural language prompts (e.g. DALL-E, Midjourney, Github Co-pilot). The reception of Generative AI has understandably been one of great excitement.

From the perspective of economic policy makers Generative AI is interesting as it appears to have the characteristics of a ‘General Purpose Technology’. That is to say, it has the potential for use in a wide range of sectors, its costs are likely to reduce overtime and it unlocks significant further innovation as it is applied in different sectors (Bresnahan and Trajtenberg, 1995)1, resulting in widespread productivity gains and boosting aggregate economic growth. Other examples of General Purpose Technologies include steam, electricity and the ICT revolution.

The potential applications of Generative AI are many and stretch across sectors, to give a few examples:

-

Customer interaction. As consumers we already interact in conversation style with computers via chatbots. However, until now it has proved very difficult to provide compelling interactions, with most chat bots limited to very small domains, matching stock answers to questions based on the frequency of particular words. This has often resulted in frustration on the part of the customer when they want answers to problems the pre-programmed list doesn’t contain and meant that customer care centres are still in wide use. Generative AI powered chatbots will enable consumers to interact in a much more human-like way, they will be able to deal with a much wider variety of questions and be able to answer with empathy.

-

Virtual Experts. Generative AI can be used by employees to access internal company information quickly and efficiently, via a ‘Virtual Expert’ with a natural language interface. For example, a Virtual Expert could enable an insurance agent or retail customer service desk agent to access policy details or product information in real time, without having to waste time mining internal information repositories using traditional search or having to build up years of prior knowledge.

-

Content creation. In creative settings Generative AI could be used for rapid ideation and to create first drafts of marketing material, reports, slide packs and social media posts; saving valuable time. It could also be used to facilitate consistency in writing style and format across a business.

-

Software and data analytics. Generative AI is able to write code in a wide variety of programming languages. In future, large parts of software will be written by Generative AI, with human programming experts undertaking debugging or completion of tasks these models are unable to handle. Similarly, data analysts and scientists will spend far less time coding models and creating charts, as Generative AI will be able to handle this. Instead these roles will be focussed on determining what are the right models to build and analyses to execute.

-

Facilitating R&D. Generative AI is already being used to produce early stage molecule designs for drug discovery. It will also be increasingly used in early stage design of many physical products. Enabling faster design and production time.

The impact of these and other applications on business productivity is not hard to imagine. If software can be written by describing desired features with natural language, rather than hiring specialist programmers to hand-write code, it will get written much quicker. If customers can have empathetic and informative conversations with GenAI chatbots, then customer service centres will be able to serve more customers, to a higher standard with fewer staff. If employees can execute research more easily, then plans and strategies will be better informed and faster to produce.

There is empirical evidence to support assumed productivity gains. Strong firm-level productivity impacts from Generative AI have been recorded by a handful of emerging research papersinto particular use cases: A recent study of 5000 customer support agents found that a Generative AI assistant improved the number of issues resolved per hour by 14% (Brynjolfsson, Li, Raymond, 2023)2. Similarly, a study of GitHub’s copilot functionality, which generates code suggestions, found that software developers using it completed tasks 56% quicker (Peng et al, 2023)3.

A more speculative genre of study estimates a significant macro-economic impact of Generative AI. These studies focus on identifying elements of existing jobs which could be replaced and from there estimate productivity gains: McKinsey (2023)4 suggests that Generative AI could add up $4.4trillion dollars to the global economy annually and boost productivity growth by 0.6 ppt, Goldman Sachs suggests twice that impact ($7 trillion and 1.5% increase in productivity growth) is achievable over a 10 year period5. These are impressive numbers.

The anticipated productivity gains from Generative AI would be nice, given the very low rates of productivity growth the developed world has been experiencing

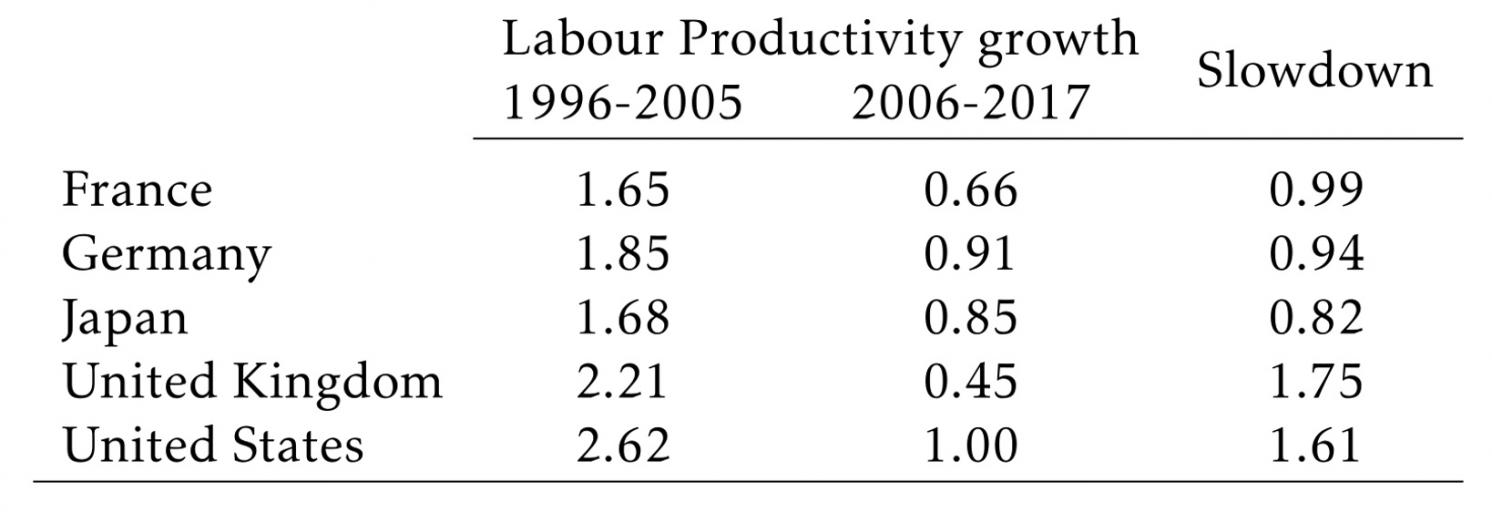

Since the early years of the millennium developed countries have experienced very low labour productivity growth (Table 1). The UK has been particularly affected, with average annual labour productivity growth falling from 2.21% over the decade from 1996-2005 to just 0.45% in the following decade.

Table 1 Labour productivity growth in five advanced economies. From Winkler et al (2021)6

Source: Winkler et al (2021). Data from EU-KLEMS 2019 (Stehrer et al. 2019).

Note: The periods for Japan (1995-2015) and the US (1998-2017) are slightly different due to data coverage.

Source: Winkler et al (2021). Data from EU-KLEMS 2019 (Stehrer et al. 2019).

Note: The periods for Japan (1995-2015) and the US (1998-2017) are slightly different due to data coverage.

This is a problem policy makers wish to solve as labour productivity growth results in increases in wages and living standards, and in the long run it is what drives economic growth. Changes in productivity also impact fiscal and monetary policy by influencing tax revenues and the rate at which an economy can grow without causing inflation, thereby influencing equilibrium interest rates. There are many theories, but little agreement, on what is behind this productivity slowdown. A simple decomposition points to the fact that in both Europe and the US, the deceleration in productivity arises mostly from a slowdown in capital deepening7 8 (i.e. lower investment in machinery used in production) and from a slowdown in Total Factor Productivity (TFP) growth (a residual term which captures introduction and diffusion of new technologies, among other things), rather than labour quality (changes to the composition of the workforce). Explanations as to why there has been a deceleration in capital deepening and in TFP growth range from measurement error, to a reduction in competition, to a loss of momentum in diversification of production and the stalling of globalisation to a slowdown in the rate of technological progress9, to name but a few theories.

The hope is that whatever the cause of current low productivity growth, Generative AI will come to the rescue.

To make an impact on aggregate productivity Generative AI will have to diffuse across the economy. History tells us that it may take many years.

There is a temptation to assume that because a technology which delivers productivity improvements exists it will be used straight away. Why would it not be? However, historical experience tells us that this is not what happens. In fact, the dominant models of technology diffusion suppose an S-shaped curve of adoption: A few adopt a technology early, once it is established the majority of firms follow leaving a minority of laggards who are late to adopt or do not adopt at all.

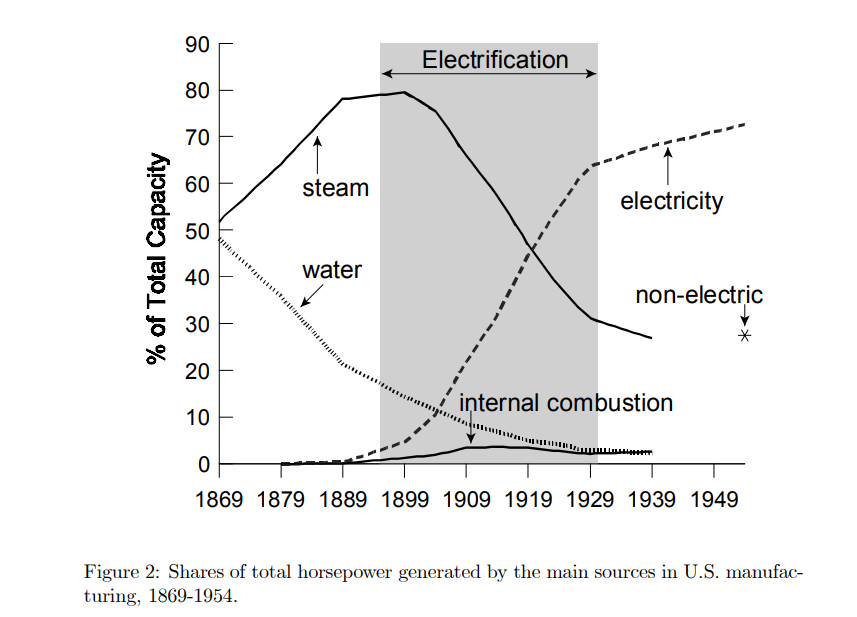

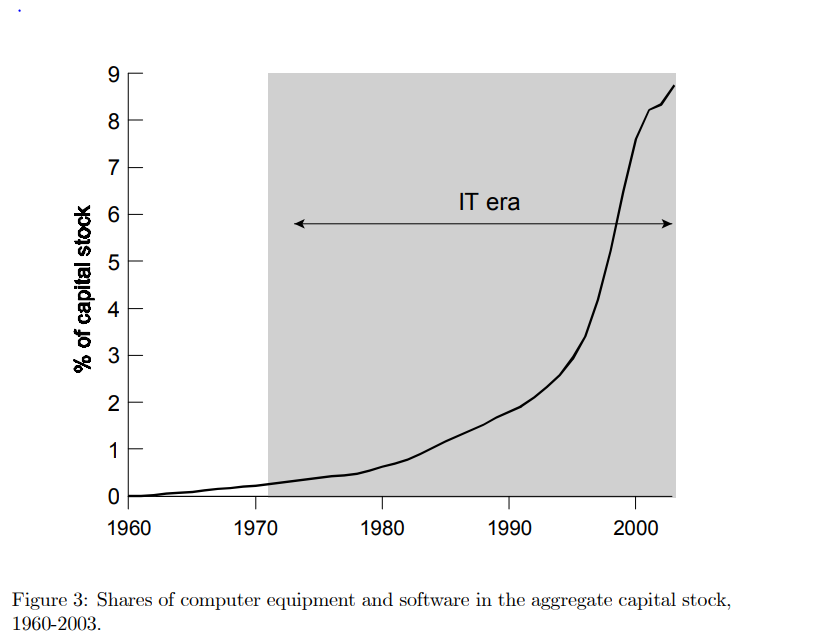

The diffusion process for General Purpose Technologies is more complex, as it leads to further innovations over time, although the pattern of diffusion is similar. However, history tells us that diffusion of General Purpose Technologies takes decades. Looking at historical examples of IT and electricity (see figures 1 and 2) Jovanic and Rousseau (2005)10 find that it took twenty years (from the opening of the first hydro-electric facility) for electricity to account for 20% of US manufacturing power usage and 15 years (from the invention of Intel’s 4004 microprocessor) for computer equipment to grow to 1% of the capital stock.

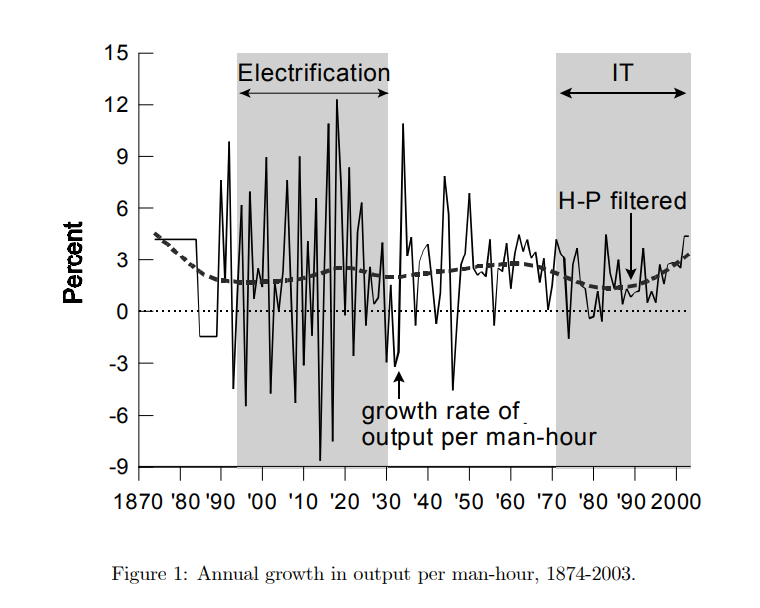

As a consequence the boost to productivity from electricity and ICT also took time to emerge. Measured increases in productivity growth not appearing for 20 years in both cases (Figure 3), leading the economist Robert Solow to famously comment that one “can see in the computer age everywhere but in the productivity statistics”.

Figure 1: Shares of total horsepower generated by main sources of U.S. manufacturing 1894-1954. From Jovanic and Rousseau (2005).

Figure 2: Shares of computer equipment and software in aggregate level capital stock 1960-2003. From Jovanic and Rousseau (2005).

Figure 3: Annual growth in output per man hour 1874-2003. From Jovanic and Rousseau (2005).

There may be a temptation to think that “this time is different” and that given that Generative AI appears to be less capital intensive and ready to use or because in today’s world things happen faster. We cannot be sure, however there are a number of things that point to the diffusion of Generative AI taking longer than many would like:

1. Gen AI will not be an “off the shelf technology” for many business use cases.

As accessible as ChatGPT may seem, Generative AI is not an “off the shelf” technology. For most use cases businesses can’t use it as it is. Tools like ChatGPT are built on so-called ‘Foundational Models’ AI models with billions of parameters trained on vast amounts of text from books and text (or images, code samples and musical fragments) from the internet. These models, which are general by nature, must then be adapted through further training or fine tuning to create applications in specific domains.

2. Firms will have to commit to significant investments to realise productivity gains

To realise gains, firms will have to invest heavily in specialist expertise, software and the right data to fine tune models along with changes to organisational structures, employee skills and ways of working.

A recent study into general AI adoption in South Korea found that firms only achieved growth when they used AI intensively with little gain to limited experimentation with the technology. It was also important that firms invested heavily in complementary technologies such as cloud computing and database systems (Choi et al 2023)11. Generative AI is unlikely to be different.

While firms make these investments there may be little or no increase in final goods produced, and hence they may not experience productivity gains for a number of years.

3. Although interest in AI in general is growing, many firms aren’t actively investing in it

Forgetting Generative AI, many firms aren’t investing in any sort of AI at the moment. This is despite the fact that Google N-grams tells us that the recent boom in interest in AI started around ten years ago12 and a number of use cases are mainstream technology by now. Only somewhere between a third and a half of global firms are actively using AI: In 2022 Mckinsey reported 50% of firms globally using AI in at least one function, white the IBM Global AI adoption index reported 35% of companies using AI. Firms who are fully exploiting AI are far fewer.

4. A significant proportion of productivity gains are likely to come from a churn of businesses

Adoption of Generative AI may be difficult for many existing firms, as it isn’t compatible with their existing production lines or technologies currently deployed, and as noted above change will require significant investment. Firms with on-premise servers with limited computing power and memory, may find it difficult to adapt to the data volumes and network speed requirement for many Generative AI use cases. Firms without a cloud computing presence or without existing applications connected to the public internet will also need a shift in the way they operate.

Firms building their business model from scratch will find it easier to build production lines with Generative AI as part of their DNA. That is likely to mean we will observe a gap in the productivity of new and established firms within a sector, with, over time, some established firms being competed out of the market. The more competitive an industry is, the faster this ‘creative destruction’ will happen.

This effect could be significant: productivity gains from reallocation of capital during the ICT revolution in the US may have been as high as 30% (Chun, Kim, Lee 2014)13.Money is already beginning to pour into new firms linked to Generative AI - Global investment by private investors in the first quarter of 2023 was $12 billion, compared to $4.5 billion for the whole of 202214. However, it will take time for these new firms to grow and established firms to exit.

5.The importance of firm management in realising productivity gains from Generative AI should not be underestimated.

Successful adoption of Generative AI will be driven by effective management decisions, both in relation to how much and where to invest, but also in how the business is transformed to make use of Generative AI. While having a CEO with previous entrepreneurial experience makes intensive investment in AI more likely15, firm wide management quality is a significant driver of the extent to which technology investments deliver productivity gains: Analysis of IT intensive industries found that nearly all of the difference in productivity between US and European owned firms is explained by management quality, specifically in “people management” that is promotions, rewards, hiring, and firing (Bloom, Van Reenan, Sadun 2016)16. Differences in management quality are likely to drive big differentials between firms in an industry as they seek to adopt Generative AI.

6. Generative AI models today have a number of technical problems giving businesses reason to be cautious.

First and foremost, Generative AI models can ‘hallucinate’, that is provide confident and coherent answers which are simply wrong. That is a significant challenge for users, particularly with sensitive use cases. While owners of foundational models are developing tools to catch hallucination, no guarantees are provided that it won’t happen.

Foundational models also change overtime, that is a risk for businesses. At present applications of Generative AI are dependent on a handful of foundational models, operated by third parties. If models change and the answers given to questions change, then it will mean the applications firms build on top of these models may start suddenly producing incorrect or undesirable results. A recent study found that ChatGPT’s performance has already deteriorated significantly in some domains. (Chen, Zaharia, Zou 2023)17

7. Generative AI presents a number of commercial legal, regulatory and ethical challenges.

Protection of confidential data and compliance with data laws is not straight forward. Access to foundational models is (mostly) offered via API, which means data has to be passed to the owner of the foundational model in order to receive the necessary response. That means it leaves the user’s domain. In some cases providers offer access on the basis that data supplied can be used for further training of models. In other cases models’ owners have used data without explicitly notifying data owners: The legitimacy of Github’s code pilot is already being tested in the courts. The tool was able to produce proprietary code, indicating it had been trained on code stored on the site which users believed to be private. There are likely to be more such legal challenges.

The black box nature of generative AI models will also cause an issue for regulators and for company ethical frameworks. Generative AI has no in-built moral compass. Without proper guard rails the output given by these models can be offensive, unpleasant, discriminatory or just plain illegal. Providers of foundational models are working very hard to limit these effects, however they cannot tailor to every domain. Firms will have to have clear processes for ensuring that any decisions which involve a Generative AI interface are clearly evidenced. For example if someone is being turned down for a loan, it will not be sufficient for a Gen AI interface to produce a yes/no answer, but it will have to be able to produce evidence for the decision.

None of these challenges are fatal to the future of Generative AI, however they do point to the fact that adoption of Generative AI and its impact on aggregate productivity will take time.

Summary and policy implications

The arrival of Generative AI is exciting and promises improvements to productivity and therefore to overall welfare. That’s good news.

However, policy makers should not be impatient for results. Interventions to promote and facilitate the adoption of Generative AI should not be closely linked to measured productivity gains over short time spans. Although adoption is in the hands of individual companies governments can facilitate the process, through:

(a) Using regulation wisely. Policy makers should allow firms to experiment with Generative AI technology without being overwhelmed with compliance. Regulation, where it is used, should also provide clarity and a level playing field for firms seeking to invest.

(b) Supporting investment in Generative AI and in complementary technologies. For example facilitating access to cloud technologies, which can be prohibitively expensive for small firms.

(c) Promoting research into Generative AI and in re-skilling of employees to use the technology.

(d)Looking into aspects of the tax and accounting regime which incentivise and disincentivise investment in technology. For example: Can the methods for accounting for intangibles be changed to allow these assets to properly appear on balance sheets and enable business to raise capital more easily?

Businesses should also be patient. They will need to be committed “all in” to reap the rewards of Generative AI, thinking of investment in Generative AI as a whole business transformation project and not just something to tinker with.

References

-

Bresnahan, T.F. and Trajtenberg, M., 1995. General purpose technologies ‘Engines of growth’?. Journal of econometrics, 65(1), pp.83-108. ↩

-

Brynjolfsson, E., Li, D. and Raymond, L.R., 2023. Generative AI at work (No. w31161). National Bureau of Economic Research. ↩

-

Peng, S., Kalliamvakou, E., Cihon, P. and Demirer, M., 2023. The impact of ai on developer productivity: Evidence from github copilot. arXiv preprint arXiv:2302.06590. ↩

-

McKinsey (2023). The economic potential of generative AI: The next productivity frontier ↩

-

Goldman Sachs (2023). Generative AI could raise global GDP by 7%. ↩

-

Winkler, Pantelis, Koutroumpis, François Lafond (2021). Re-evaluating the sources of the recent productivity slowdown. VoxEU. ↩

-

ECB (2016). The slowdown in US labour productivity growth – stylised facts and economic implications. ↩

-

ECB (2021). Key factors behind productivity trends in euro area countries ↩

-

https://www.nature.com/articles/s41586-022-05543-x ↩

-

Jovanovic, Boyan and Rousseau, Peter L., General Purpose Technologies (January 2005). NBER Working Paper No. w11093, Available at SSRN: https://ssrn.com/abstract=657607 ↩

-

https://www.sciencedirect.com/science/article/abs/pii/S0166497222001377 ↩

-

Google N-grams. https://books.google.com/ngrams/graph?content=AI%2C+artificial+intelligence&year_start=1800&year_end=2019&corpus=en-2019&smoothing=3 ↩

-

Chun, H., Kim, J.W. and Lee, J., 2015. How does information technology improve aggregate productivity? A new channel of productivity dispersion and reallocation. Research Policy, 44(5), pp.999-1016. ↩

-

Pitchbook (2023). The most active investors in generative AI. https://pitchbook.com/news/articles/top-generative-ai-vc-investors-list ↩

-

Lee, Y.S., Kim, T., Choi, S. and Kim, W., 2022. When does AI pay off? AI-adoption intensity, complementary investments, and R&D strategy. Technovation, 118, p.102590. ↩

-

Bloom, N., Sadun, R. and Reenen, J.V., 2012. Americans do IT better: US multinationals and the productivity miracle. American Economic Review, 102(1), pp.167-201. ↩

-

Chen, L., Zaharia, M. and Zou, J., 2023. How is ChatGPT’s behavior changing over time?. arXiv preprint arXiv:2307.09009. ↩